Emergency Fund Account Comparison Tool

Your Emergency Fund Needs

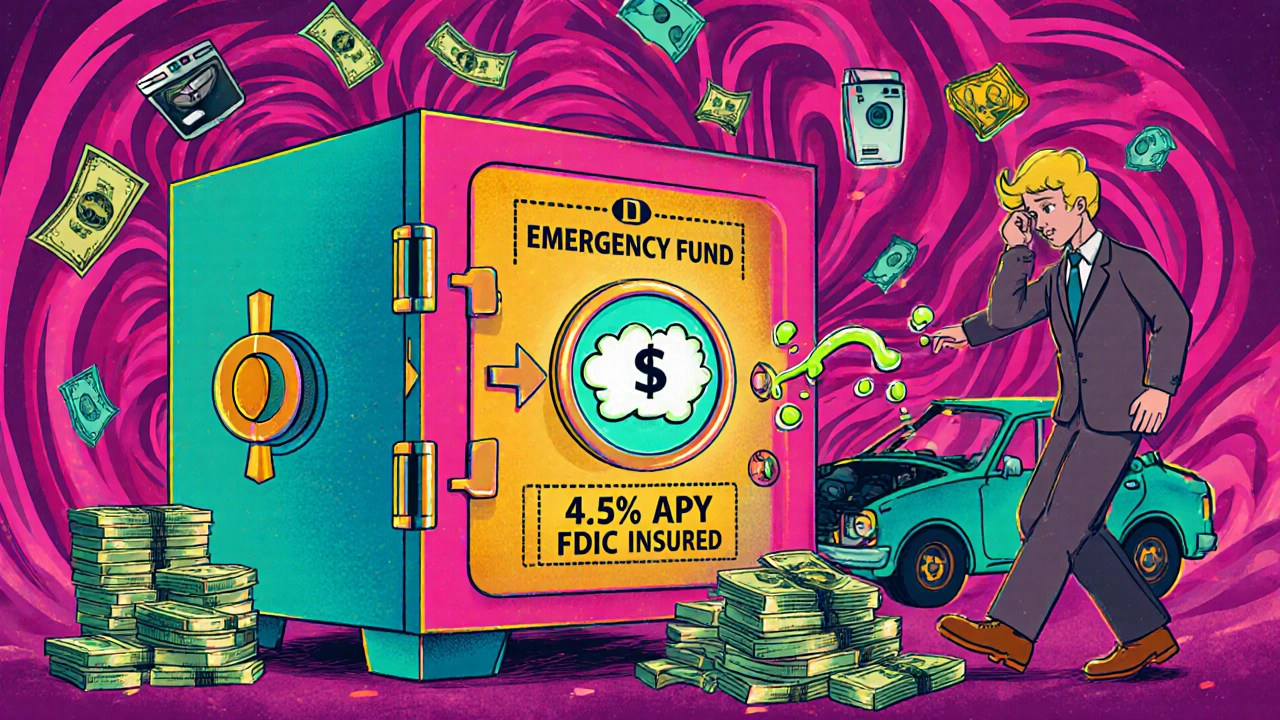

When your car breaks down, your fridge dies, or your paycheck gets delayed, your emergency fund is the only thing standing between you and a credit card bill you can’t pay. But here’s the thing: emergency fund isn’t just about how much you save - it’s about whether you can actually get to that money when you need it. Too many people stash cash in places that sound safe but lock it away when disaster strikes. That’s not an emergency fund. That’s a savings account with a penalty clause.

What Makes an Emergency Fund Work?

An emergency fund isn’t meant to grow rich. It’s meant to keep you from going broke. The Consumer Financial Protection Bureau (CFPB) found that the average household faces more than one financial shock per year - a medical bill, a broken appliance, a sudden job gap. And the median size of those shocks? About three weeks of income. That’s why experts say one month’s worth of essential expenses is the bare minimum. If you’re earning $3,000 a month, that’s $3,000 in cash you can touch without asking permission. The real question isn’t how much you save. It’s: Where is it? If you can’t access it within 24 hours, it doesn’t count as emergency-ready. And if you’re losing money to fees or penalties just to get it out, you’re doing it wrong.High-Yield Savings Accounts: The Gold Standard

If you want one option that checks every box - safety, speed, and decent returns - go with a high-yield savings account (HYSA). As of Q3 2024, these accounts are paying between 4.00% and 5.50% APY. That’s 10 to 15 times what you’d earn at a traditional bank. And here’s the kicker: your money is FDIC-insured up to $250,000. If the bank fails, the government covers you. You can withdraw money anytime. No penalties. No waiting. Just log in, click “transfer,” and the funds hit your checking account in one to two business days. Some online banks like Ally and Marcus by Goldman Sachs even let you do instant transfers to linked accounts. Most don’t require a minimum balance. No hidden fees. No complicated rules. And you can set up automatic transfers from your paycheck - Fidelity found people who automate save 2.3 times more than those who do it manually. That’s the secret sauce: make it effortless. Reddit users in r/personalfinance overwhelmingly pick HYSA as their primary emergency fund. Why? Because when your dog needs emergency surgery and you need $1,200 by tomorrow, you don’t want to call your bank, wait for a wire, or pay a penalty. You just want the money.Money Market Accounts: A Step Up in Flexibility

Money market accounts (MMAs) are like HYSA’s slightly fancier cousin. They also pay 3.50% to 5.00% APY and are FDIC-insured. But they come with extra features: check-writing and debit card access. That means you can pay a plumber directly from your emergency fund without transferring to checking first. That sounds great - until you hit the limits. Federal rules (Regulation D) still cap you at six convenient withdrawals per month. That includes transfers, online payments, and debit card purchases. If you go over, you get charged $10-$25 per extra transaction. Some banks even freeze your account or convert it to a regular checking account. Bankrate users in early 2024 reported frustration when they had to pay multiple fees after two car repairs in one quarter. “I thought I was being smart with a money market account,” one user wrote. “Turns out I was just paying for the illusion of flexibility.” MMAs make sense only if you’re confident you won’t need more than five withdrawals a year. If you’re the kind of person who uses their emergency fund for small, frequent surprises - like replacing a broken phone or fixing a leaky roof - stick with a HYSA.

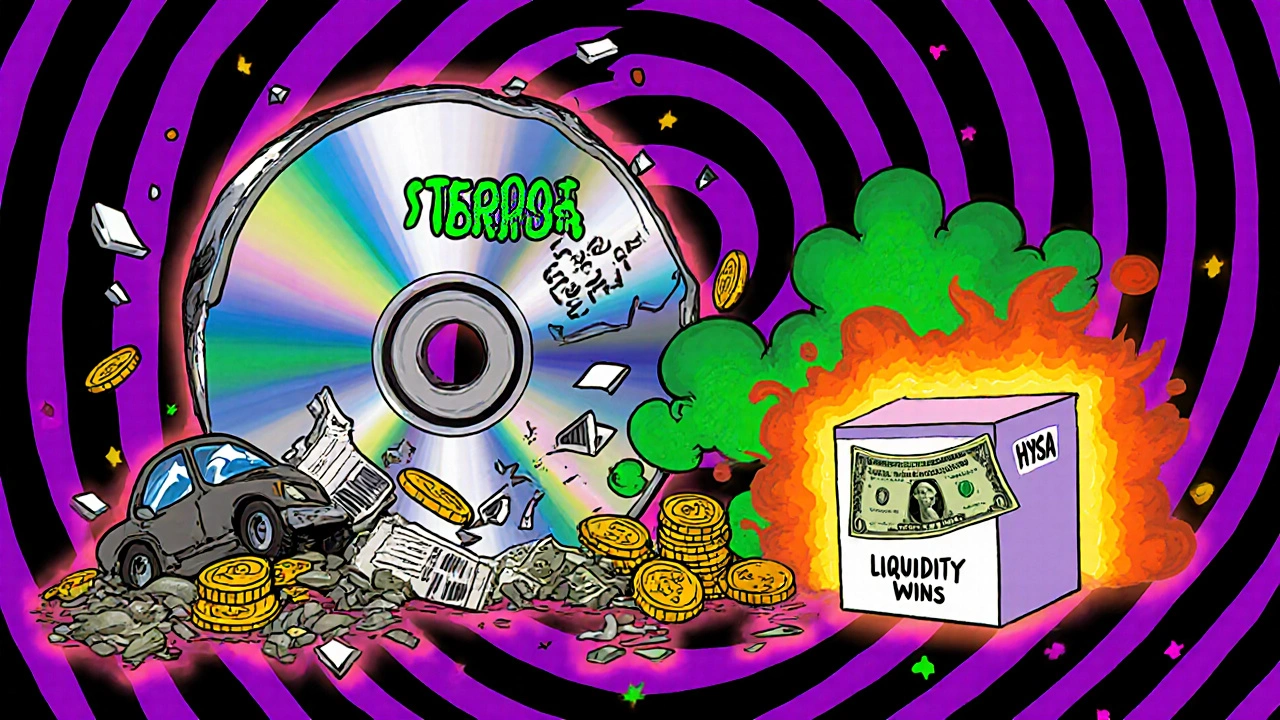

Certificates of Deposit: The Trap of Higher Rates

CDs promise higher interest. A 12-month CD might pay 5.50% APY - that’s 0.5% more than a top HYSA. Sounds tempting, right? Here’s the catch: you can’t touch the money until the term ends. If you do, you pay a penalty. Experian’s September 2025 report found most penalties equal 3 to 6 months of interest. On a $5,000 CD earning 5.5%, that’s $68 to $137 in lost earnings. Consumer Affairs reviews from 2024 show 86% of people who used CDs for emergency funds ended up moving the money out. Why? Because emergencies don’t wait. One person’s car broke down. They cashed out a 3-month CD early. The penalty? $127. The extra interest they earned? $38. You’re paying more to lose more. CDs have a place - but not in your emergency fund. Use them for goals you’re 100% sure about: a vacation next summer, a down payment in 18 months. Not for “just in case.”Treasury Bills: Government Backing, Market Risk

Treasury Bills (T-Bills) are backed by the U.S. government. They’re safe from bank failure. But they’re not safe from market swings. You buy a T-Bill for, say, $1,000 with a 5.2% yield that matures in 13 weeks. But if interest rates rise while you’re holding it, the market value of your T-Bill drops. If you need cash before maturity and sell it early, you might get less than you put in. NerdWallet warns against this for emergency funds. “You’re trading bank insurance for market risk,” they say. And in an emergency, you don’t want to gamble on whether your money will be worth what you expected. Plus, buying T-Bills isn’t as simple as opening a bank account. You need a TreasuryDirect account or a brokerage. Selling them means placing a market order - not a click-and-transfer. T-Bills are great for short-term investing. But they’re not for emergencies.What About Stocks, ETFs, or Mutual Funds?

Don’t. NerdWallet, Vanguard, and Experian all agree: never use volatile investments for emergency savings. The stock market can drop 10% in a week. If your car dies and you need $2,000, you can’t wait for the market to recover. You need cash now. One person in a 2024 financial forum said they invested $4,000 in an S&P 500 ETF for their emergency fund. When their furnace failed, the market was down 8%. They had to sell at a loss - and still owed $1,200 on their credit card. Emergency funds are not investments. They’re insurance. You don’t buy car insurance hoping to make money. You buy it so you don’t go bankrupt when something breaks.

How to Build It Right

Start small. Even $500 helps. The CFPB found that households with just one month of income saved saw 47% fewer negative financial events during emergencies. Set up automatic transfers. Have $50 or $100 come out of your paycheck and go straight into your HYSA. Do it on payday. Out of sight, out of mind. Keep it separate. Don’t link your emergency fund to your debit card. Make it a little harder to spend. You want friction - not convenience - when it comes to dipping in. Aim for 3-6 months of essentials. Rent, utilities, groceries, insurance, transportation. Not Netflix. Not dining out. Just survival. If you have more than $250,000 saved, split it across two FDIC-insured banks. That’s the legal limit per bank. Don’t risk losing a dime.What to Do If You’ve Already Made a Mistake

If your emergency fund is locked in a CD or buried in stocks, don’t panic. Just start over. Open a new HYSA today. Even if it’s just $100. Then, move your next paycheck into it. Keep adding until you’ve rebuilt. Once you’ve got a solid cushion, then consider moving the old money out - pay the penalty if you have to. Better to lose $100 now than risk losing $1,000 later. The October 2025 federal shutdown showed how quickly emergencies hit. Over 40% of federal workers used their emergency savings within two weeks. Most had HYSA accounts. Those who didn’t? They were scrambling.Final Rule: Liquidity Wins

The best emergency fund isn’t the one with the highest interest rate. It’s the one you can access without stress, without fees, without waiting. High-yield savings accounts win because they combine safety, speed, and solid returns. No tricks. No fine print. Just cash when you need it. Everything else - MMAs, CDs, T-Bills, stocks - has trade-offs that don’t belong in an emergency fund. They’re for goals with timelines. Not for surprises. Your emergency fund isn’t about being smart with money. It’s about being ready for life.Can I use my checking account as an emergency fund?

You can, but you shouldn’t. Checking accounts usually pay 0.01% to 0.10% APY - you’re losing purchasing power to inflation. Plus, it’s too easy to spend. Your emergency fund needs to be separate, with a little friction to prevent accidental use. A high-yield savings account is the better choice - same access, better returns.

How much should I have in my emergency fund?

Start with one month of essential expenses - rent, groceries, utilities, insurance, transportation. Once you’ve got that, aim for three to six months. The CFPB found that households with at least one month saved are 47% less likely to face serious financial trouble during an emergency. If you’re self-employed or have an unstable income, aim for six months or more.

Is it safe to keep my emergency fund in an online bank?

Yes, as long as the bank is FDIC-insured. Online banks like Ally, Marcus, and Capital One offer the same federal protection as big brick-and-mortar banks. In fact, they often pay higher interest because they have lower overhead. Just verify the bank’s FDIC status on the official FDIC website before opening an account.

Should I use a money market fund instead of a money market account?

A money market account (MMA) is FDIC-insured and safe. A money market fund is a type of mutual fund - not insured, and its value can fluctuate. Vanguard and NerdWallet warn against using funds for emergency savings. Stick with MMAs from banks or credit unions. Avoid brokerage-based money market funds unless you fully understand the risk.

What if I lose my job and need to use my emergency fund?

That’s exactly what it’s for. Use it. Don’t feel guilty. The goal is to avoid debt. Once you’ve used part of it, focus on rebuilding. Start by saving a small amount from each paycheck - even $25 a week adds up. Don’t wait until you’re back to full income. Rebuilding is part of the process.

Can I have multiple emergency funds?

Yes, and it’s smart. Some people keep a small, ultra-liquid fund ($1,000-$2,000) in a checking account for immediate needs like a flat tire. Then they keep the rest in a HYSA for bigger emergencies. This gives you both speed and growth. Just make sure the main fund is in a safe, interest-earning account.

Julia Czinna

October 31, 2025 AT 19:18I used to keep my emergency fund in a CD because I thought higher interest = smarter. Then my dog got sick and I had to cash out early-lost $92 in penalties, and the vet bill was $1,100. I learned the hard way that liquidity isn’t a feature, it’s the point. Now I use Ally’s HYSA. Instant transfers, no fees, and I’m earning 5.2%. No regrets.

Also, never link it to your debit card. I made that mistake once. Turned out ‘emergency’ just meant ‘I wanted coffee and a new pair of shoes.’

Laura W

November 1, 2025 AT 09:34Y’all are overcomplicating this. HYSA = emergency fund. Period. MMAs? Nice if you’re a financial nerd who counts withdrawals like a librarian. CDs? That’s not an emergency fund-that’s a ‘I’m gonna regret this later’ fund.

And T-Bills? Bro, you’re trying to hedge against inflation with a tool that *is* inflation-sensitive. That’s like using a paper umbrella in a hurricane. Stick with FDIC. Stick with HYSA. Stick with sanity.

Also-automate it. $75 from every paycheck. No thinking. No willpower. Just money moving while you sleep. That’s how you build wealth without trying.

RAHUL KUSHWAHA

November 3, 2025 AT 09:20Good post. I live in India, and here banks don’t even offer HYSA like in US. But I opened a US-based online account with Ally using my NRI status. Took 3 weeks to verify, but now I get 5.1% APY. Worth it.

My emergency fund is $2,000-split: $500 in local savings (for quick needs like rickshaw fare or phone repair), rest in HYSA. Simple. Safe. Smart. 😊

Graeme C

November 3, 2025 AT 19:02Let me be brutally honest: if you’re still debating whether to use a money market account over a high-yield savings account, you’re not ready for an emergency fund-you’re ready for a financial therapy session.

Regulation D? Six withdrawals? You think you’re being clever by having check-writing access? Nah. You’re just setting yourself up for fees, account freezes, and the kind of rage that makes you scream into a pillow at 2 a.m. when your fridge dies and you can’t touch your own money.

HYSA is the only option that doesn’t make you beg for access. It’s not sexy. It’s not flashy. It’s not a ‘get rich quick’ scheme. It’s the financial equivalent of a seatbelt. You don’t wear it because you want to-you wear it because you’re not an idiot.

And if you’re putting emergency money in stocks? You’re not investing. You’re gambling. And your emergency fund isn’t a casino-it’s your lifeline. Treat it like one.

Open the account. Set the auto-transfer. Forget it exists. And when the universe hits you with a $1,500 bill? You’ll thank yourself. Not the bank. Not the algorithm. YOU.